Glossary

Investment ManagementTheta

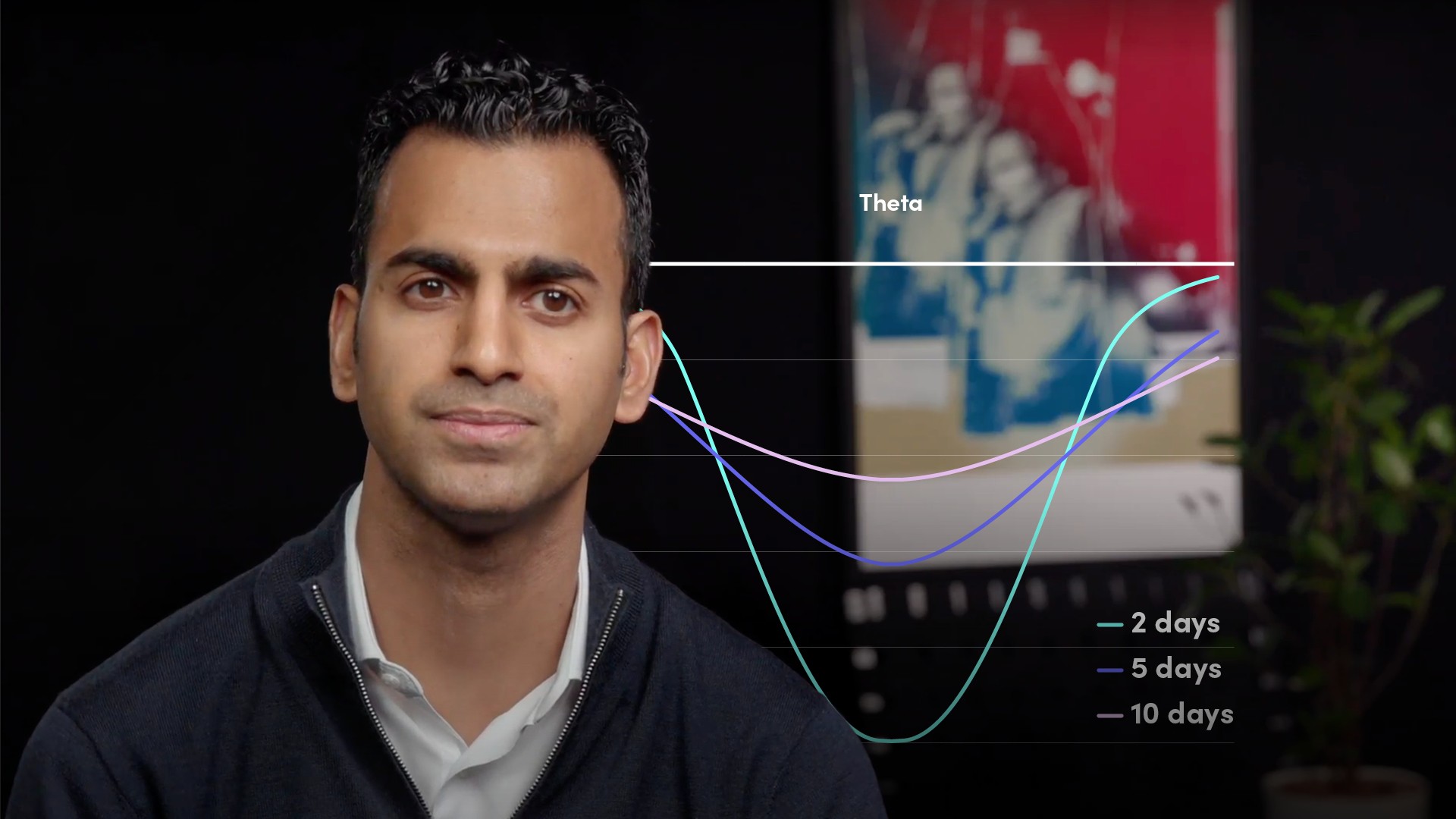

Theta is an options Greek that measures the time sensitivity of an option i.e. an option’s time decay. It represents how the price of an option declines relative to time hence is denoted as a negative number. Theta is not linear or constant; it increases as time to expiry reduces given that at expiry, an option no longer has any sensitivity to time.