Glossary

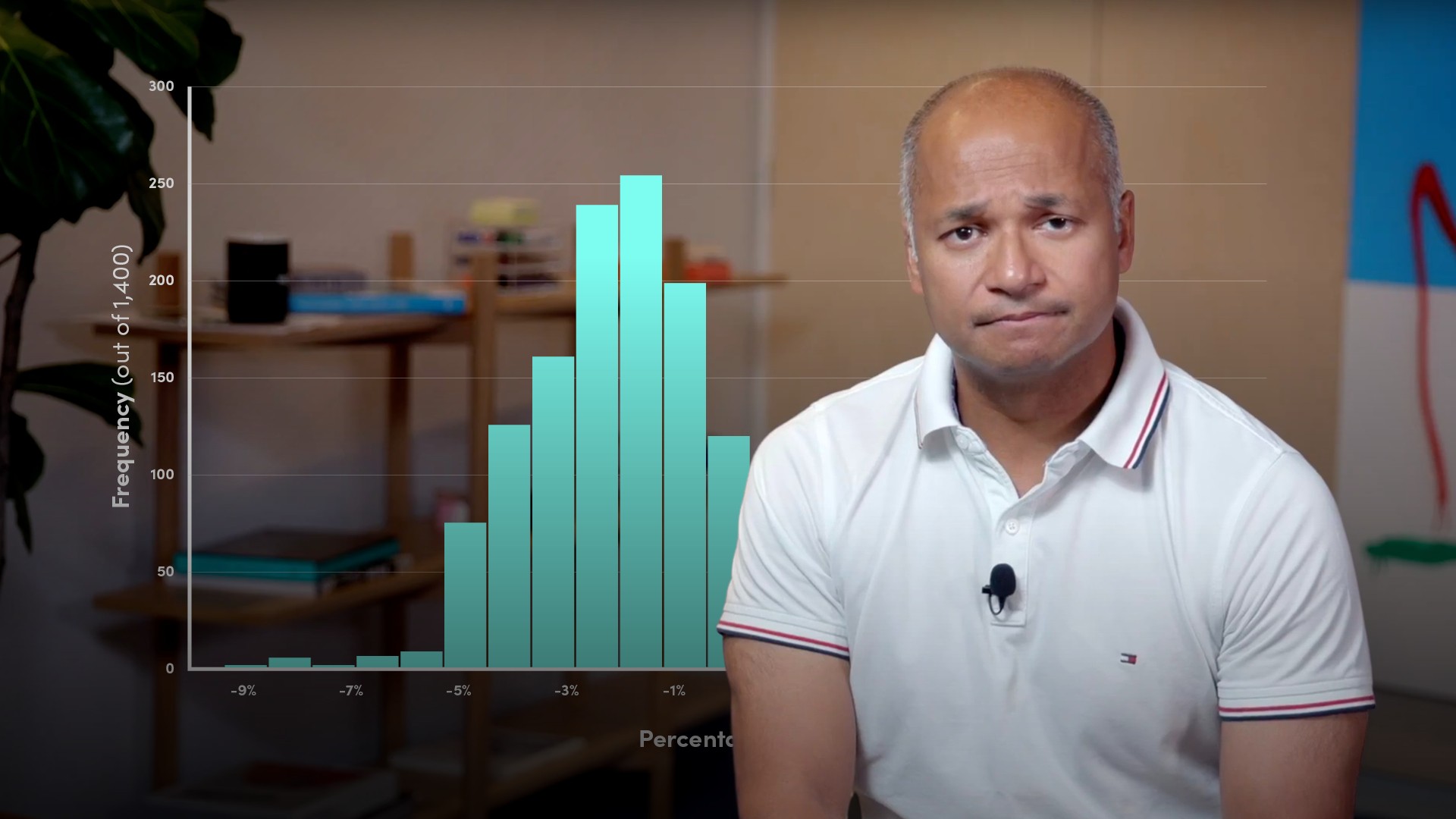

Investment ManagementValue at Risk (VaR)

Value-at-Risk is a quantitative tool widely used within financial institutions and investment firms. It calculates the downside risk of a position or series of positions and the probability of the maximum risk of loss actually occurring over a given time horizon. Risk managers use VaR among other metrics to set the firm’s risk parameters and ensure sufficient loss reserves are in place and capital buffers are maintained.