Glossary

BankingWeighted Average Rating Factor

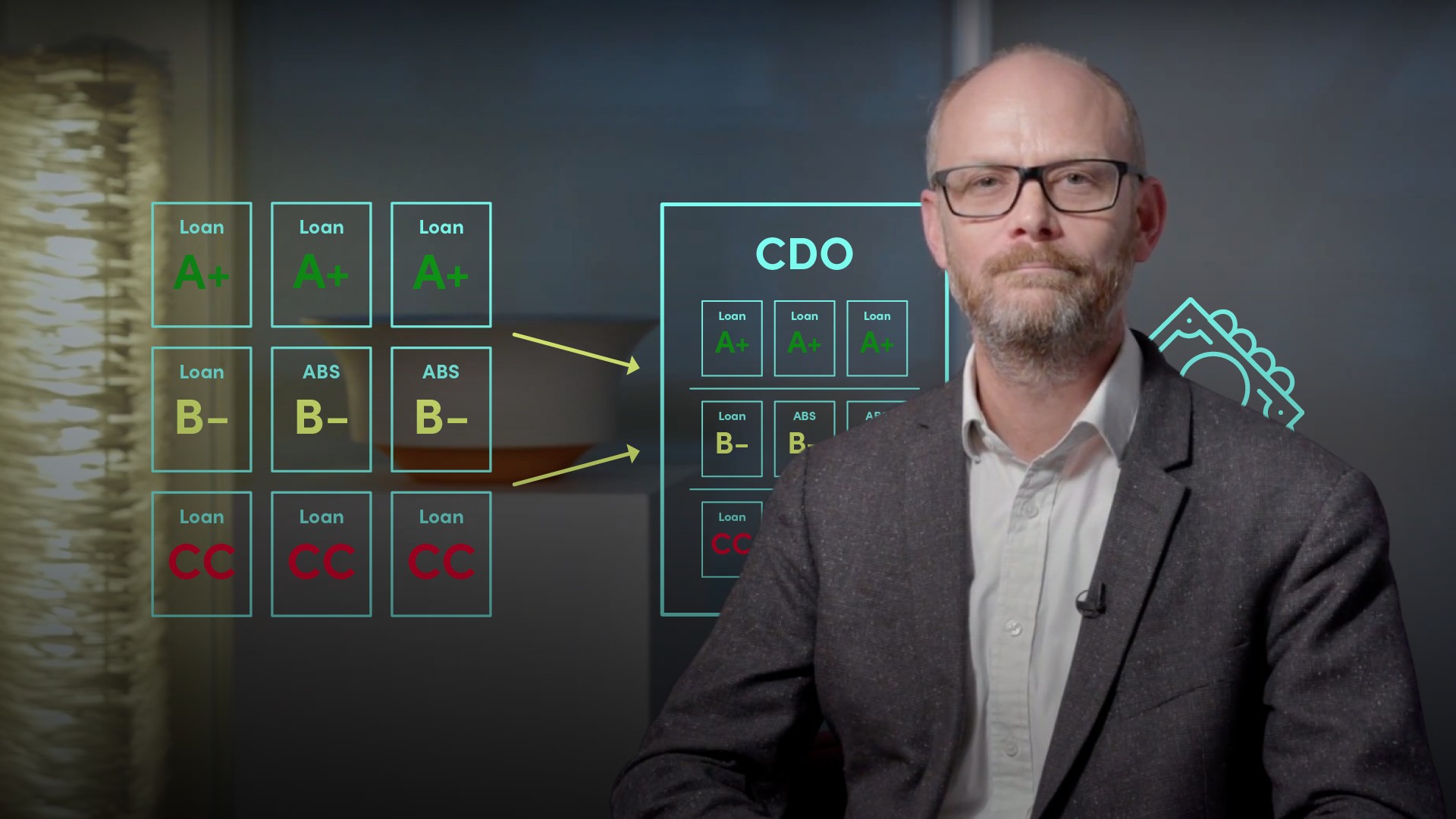

The Weighted Average Rating Factor (WARF) is a rating agency measure of the credit risk of a credit portfolio (including CLOs and CDOs) where the credit risk of each holding is weighted by its credit rating. Applying WARF gives a credit score for the portfolio based on the weighted average ratings of underlying holdings and is a useful gauge of the riskiness of the portfolio from the perspective of likelihood of repayment. Moody’s applies a numerical rating factor to every rating in its scale, including +/- notches. Aaa has a rating factor of 1, Aa1 has a rating factor of 10, Aa2 has a rating factor of 20 and so on all the way to Ca-C, which has a rating factor of 10,000.