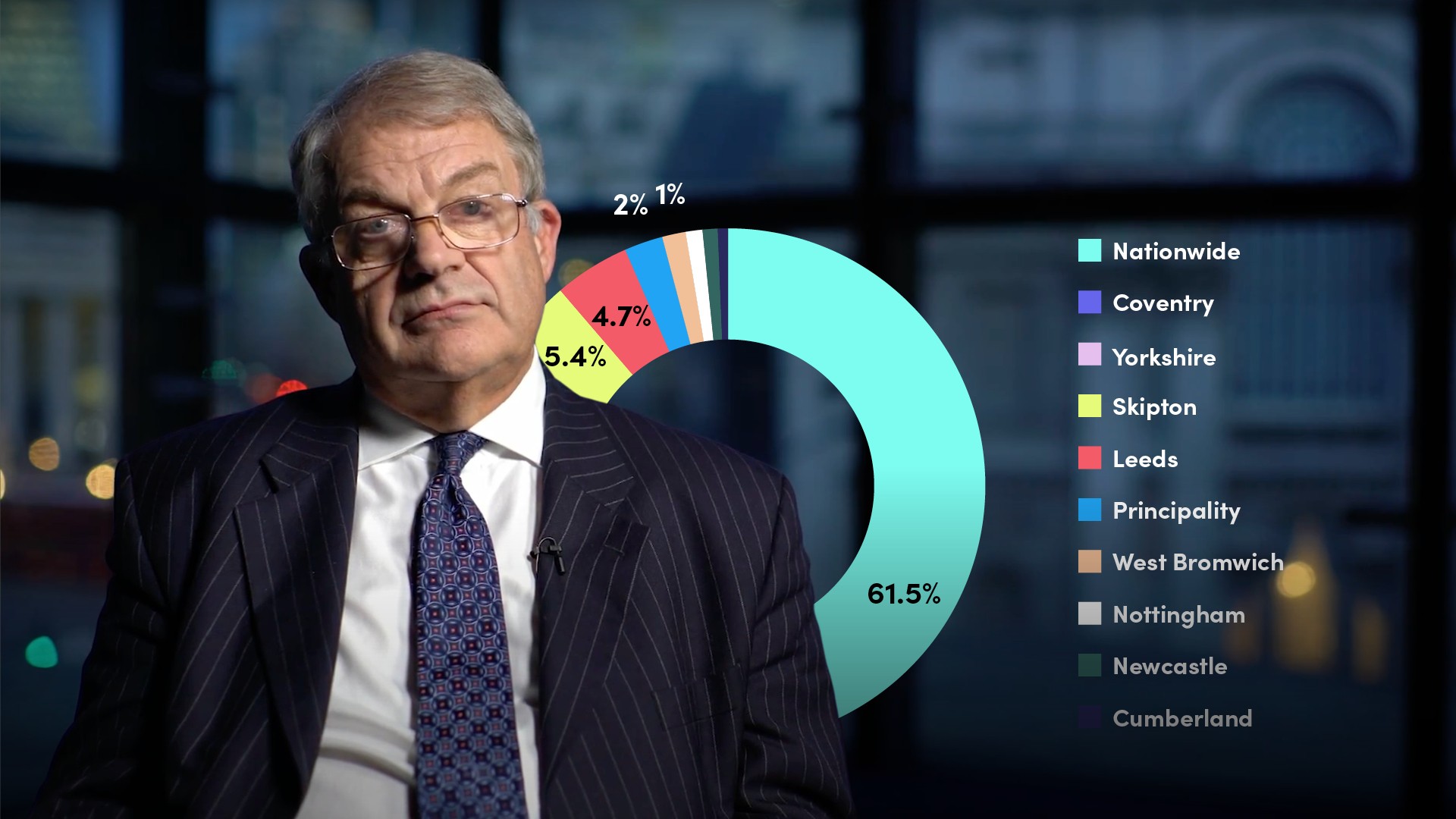

Overview and History of Building Societies

Sir Mark Boleat

40 years: Executive leadership & banking

Building societies have evolved into specialist savings banks which concentrate on mortgage lending. In the first video of the series on building societies, Sir Mark Boleat explains the evolution of these financial institutions in order to understand their place in the British system today.

Building societies have evolved into specialist savings banks which concentrate on mortgage lending. In the first video of the series on building societies, Sir Mark Boleat explains the evolution of these financial institutions in order to understand their place in the British system today.

Overview and History of Building Societies

9 mins 40 secs

Key learning objectives:

Understand why building societies grow in popularity

Outline the five key features of the 1986 Building Societies Act

Understand why converting building societies struggled in financial markets

Overview:

Building societies originated as societies of people seeking to build their own homes, and since evolved into specialist savings banks, concentrating on retail savings and mortgage lending. However, shortly after converting to PLC status, many building societies were acquired by larger banks.

What was the core purpose of building societies?

The members, generally artisans, and typically no more than 20, paid an agreed sum into the society fortnightly or monthly. When sufficient money had accumulated, land was bought and building of houses commenced. Members continued making payments until all the members had been housed, and the society then terminated.How did the growth of building societies change over time?

- The first known building society was established in Birmingham in 1775, and by the end of the 18th century, as many as 50 had been established

- In the early 19th century, to speed up the production of houses, some societies began to pay interest to people willing to invest, but who did not want a house

- The Regulation of Benefits Building Societies Act 1836 gave building societies official recognition and made provision for the registering of societies’ rules

- The 1874 Building Societies Act provided a comprehensive framework for societies that largely remained in place for over 100 years

- In 1895, it is estimated that there were 3,642 societies with a total of 631,000 shareholders, that is, investors and total assets of £45m

- By the end of 1939, the number of societies had fallen to under 1,000, but there were over 2m shareholders, 1.5m borrowers and total assets of £773m

- A 1960 Act gave the regulator, the Chief Registrar of Friendly Societies, greater powers, particularly in respect of liquid funds

- A 1962 Act consolidated existing legislation and remained in place until 1986

- In the mid-1970s, a severe housing market recession helped to focus public attention on the building societies, which had become more synonymous with the mortgage market

Why did building societies grow in popularity?

- Building societies were seen as small, specialist organisations, owned by their customers. They were not subject to the same attention from analysts as were companies listed on the Stock Exchange.

- During the 1960s and 70s, they came more into the public eye. This was partly because balance sheet restrictions on the banks in effect left the rapidly growing savings and mortgage markets to the building societies.

- They rapidly increased their business and particularly their share of the liquid savings market.

- By the early 1980s, building societies dominated the mortgage market and the retail savings market, partly due to the constraints on banks

What were the five key features of the 1986 Building Societies Act?

- The Building Societies Commission was established to be responsible for the supervision of building societies. This represented a change from the previous arrangement whereby a single person was the regulator

- The nature of the building society was defined by quantitative limits relating to assets and liabilities. The Act provided that 80% of funds had to be raised from retail sources, and that 90% of commercial assets had to be in first mortgage loans to owners of residential property

- Societies were given wider powers, including the ability to make unsecured loans to own land, although only 5% of commercial assets could be in these new classes of business

- The mutual status of building societies remained unchanged, although members were given greater powers, including the right of borrowers to vote on mergers as well as investors

- Provision was made for the building societies to convert to company status with the agreement of members

Which societies first converted into company status?

- This provision was written in the 1986 Act for Building Societies, however, didn’t go as planned. This actually led to people joining societies solely with the intention of benefitting from any windfall payment in the event they converted or were acquired by a bank

- Initially, the Abbey National formally became a public limited company, regulated as a bank in 1989. The next conversion was in 1994, others soon followed - and in 1997, the largest building society - the Halifax converted

Why did converting building societies struggle in financial markets?

They lacked expertise other than in their mainstream functions of retail savings and mortgage lending. Over time, all of the building societies that converted were acquired by banks:

- The Abbey National was acquired by Santander, the Spanish bank in 2004

- Halifax merged with the Bank of Scotland in 1999, forming HBOS. Subsequently, following the financial crisis, it became part of the Lloyds Banking Group, although it still trades as the Halifax

Sir Mark Boleat

There are no available Videos from "Sir Mark Boleat"