Credit Spread Risk in the Banking Book (CSRBB)

Moorad Choudhry

35 years: Banking and Capital Markets

In this video, Moorad demystifies the credit spread risk in the Banking Book (CSRBB), a crucial factor for banks. He covers its basics, regulatory requirements, practical application, and relevance in today's banking landscape. Join us to understand how CSRBB impacts financial institutions and their risk management strategies.

In this video, Moorad demystifies the credit spread risk in the Banking Book (CSRBB), a crucial factor for banks. He covers its basics, regulatory requirements, practical application, and relevance in today's banking landscape. Join us to understand how CSRBB impacts financial institutions and their risk management strategies.

Credit Spread Risk in the Banking Book (CSRBB)

14 mins 14 secs

Key learning objectives:

Understand the concept of credit spread risk in the banking book and what impact it has

Outline CSRBB regulatory requirements

Understand the application of CSRBB in practice

Understand the overlap between CSRBB and other regulatory and accounting regimes

Overview:

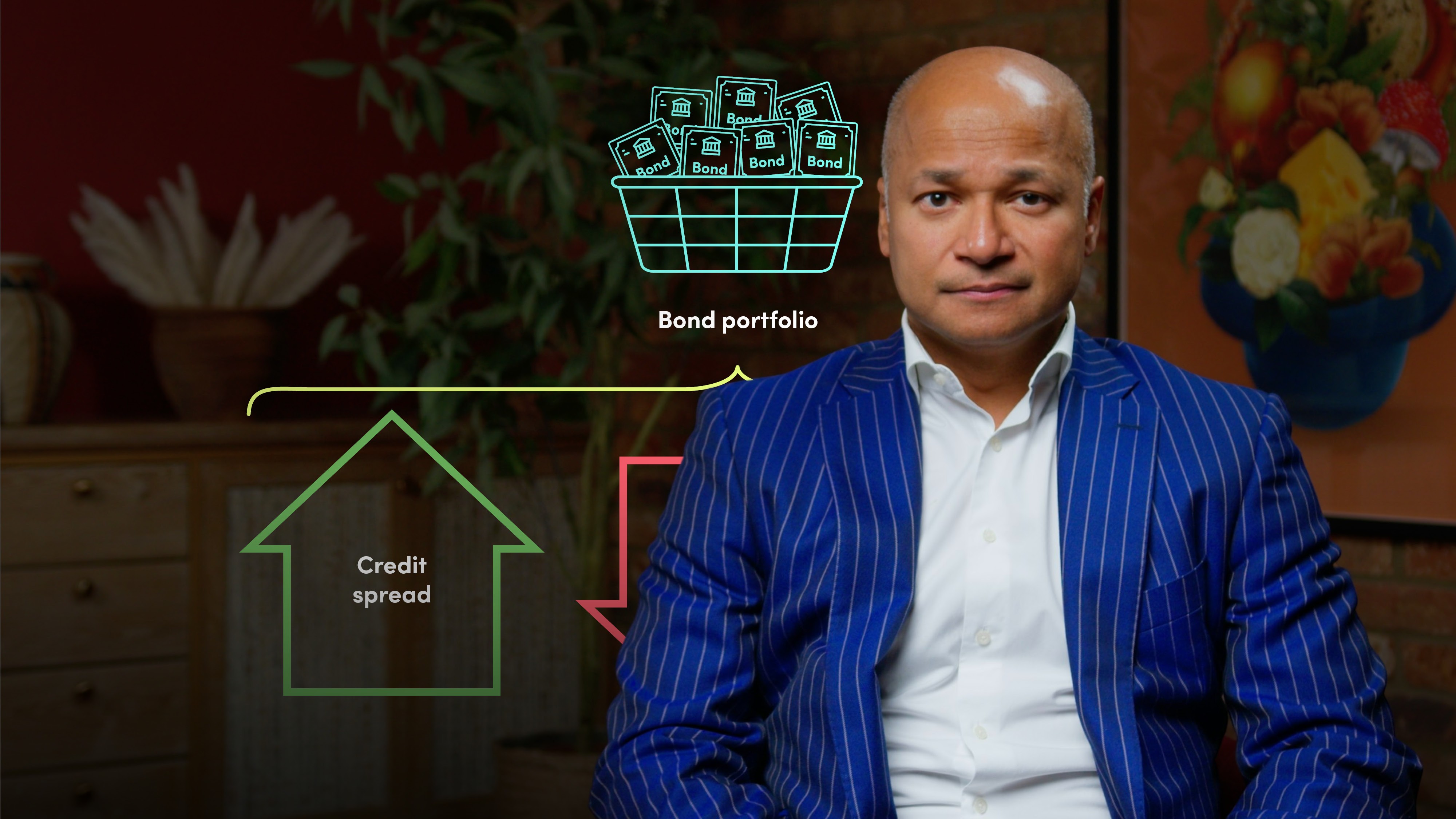

Credit Spread Risk in the Banking Book (CSRBB) pertains to how credit spread changes influence a bank's financial instrument values, notably within its banking book for long-term assets. Instruments like bonds are sensitive to these fluctuations; for example, a wider spread might lower a bond's value. This was underscored by Silicon Valley Bank's 2023 issues from US Federal Reserve rate hikes. Banks with significant bond portfolios need to be especially vigilant of CSRBB and monitor their exposures. The Basel guidance emphasises that banks must manage both interest-rate and credit-spread risks. For banks, CSRBB chiefly impacts bond portfolios, with the EBA noting that changes in credit spread at the portfolio level should be evaluated. The practical application focuses on a bank's bond holdings, especially those under Fair Value through Other Comprehensive Income (FVOCI) rules. Yet, the inclusion criteria for CSRBB remain debated, as does its overlap with IFRS 9 accounting.

Moorad Choudhry

There are no available Videos from "Moorad Choudhry"