Futures and Forwards Pricing

Gontran de Quillacq

25 years: Derivatives trading & ETFs

In this video on this series, Gontran explains the pricing of futures and forwards, the repo adjustment and finally finishes by introducing the ISDA master agreement.

In this video on this series, Gontran explains the pricing of futures and forwards, the repo adjustment and finally finishes by introducing the ISDA master agreement.

Futures and Forwards Pricing

14 mins 22 secs

Key learning objectives:

Define Forward contracts

Define Repo

Outline the factors that determine the fair value of an asset

Understand how the Delta of forwards and futures is expressed

Define the ISDA master agreement

Overview:

In this video, Gontran explains the pricing of futures and forwards, the repo adjustment and introduces the ISDA master agreement.

What are Forward contracts?

An agreement, executed now, to buy a given asset at a certain price in the future.

So, if we take a look at a security such as a firm stock, when you purchase a stock on a forward basis. You pay the cash in one year and you receive the share in one year. So, between now and then, the cash will remain in your bank account, and the share will remain in the custodian account of your counterparty.

The seller can use that share and he or she will collect any stock lending fees during the period. More significantly, he or she will continue to receive and keep the dividends deducted by the firm throughout the same period. If the asset was a bond, the owner will keep the coupons issued by the issuer of the bond. You have the advantage of retaining the cash in your account and hence maintaining the interest that has been collected on it.

What is Repo?

A slight adjustment of the fair value for the benefits incurred before settlement.

Where does Repo come from?

Repo comes from ‘repurchase rate’. A lending practice where you ‘sell and repurchase’ an asset and that pro generates cash in your bank account. Sales and repurchase rates are uncommon in the equity market, and they happen for cash generating or guaranteed stock lending purposes. When you want the asset to be physically present in your account.

Repo in different asset classes

- In the foreign exchange world, outside some very rare exceptions when you have an offshore situation where cash is restricted there is no repo in foreign exchanges.

- In the bond market for high-grade assets, there is a tiny repo. There are many treasury bills, and virtually no benefit in having one vs another and all bonds have virtually the same repo rate.

- In the equity space, the benefit of repo can come from several factors:

- It can create lending value in the inventory, so it is stock specific - some stocks are extremely difficult to borrow and you might want to pay to have that stock in your inventory so you have a very negative repo.

- It is also highly sensitive to the quality of the stock received as collateral by the cash lender. A Dow component is far superior collateral to a small-cap stock from the bottom of the Russell 2000, or a stock from Mexico or Peru.

- Equity repo is also a rare result of mistakes in interest rate calculation, therefore there is a little discrepancy in the world of LIBOR, the way LIBOR is gathered, not all banks are defining the computation of LIBOR.

- In commodities space the Repo is a very significant aspect of the fair value calculation and it’s a very volatile component of the fair value calculation.

What factors determine the fair value of an asset?

- The current price of the asset (spot)

- The cost of borrowing money (funding)

- The benefit of having the asset with you, or the cost of storing it

- An adjustment called the 'repo' which takes into account all other things we haven't taken into account

How is the Delta of forwards and futures expressed?

The Delta of the Forward is expressed as:

Dforward = 1 + repo * T

While the delta of the futures is

DFutures = 1 + (R+repo) * T

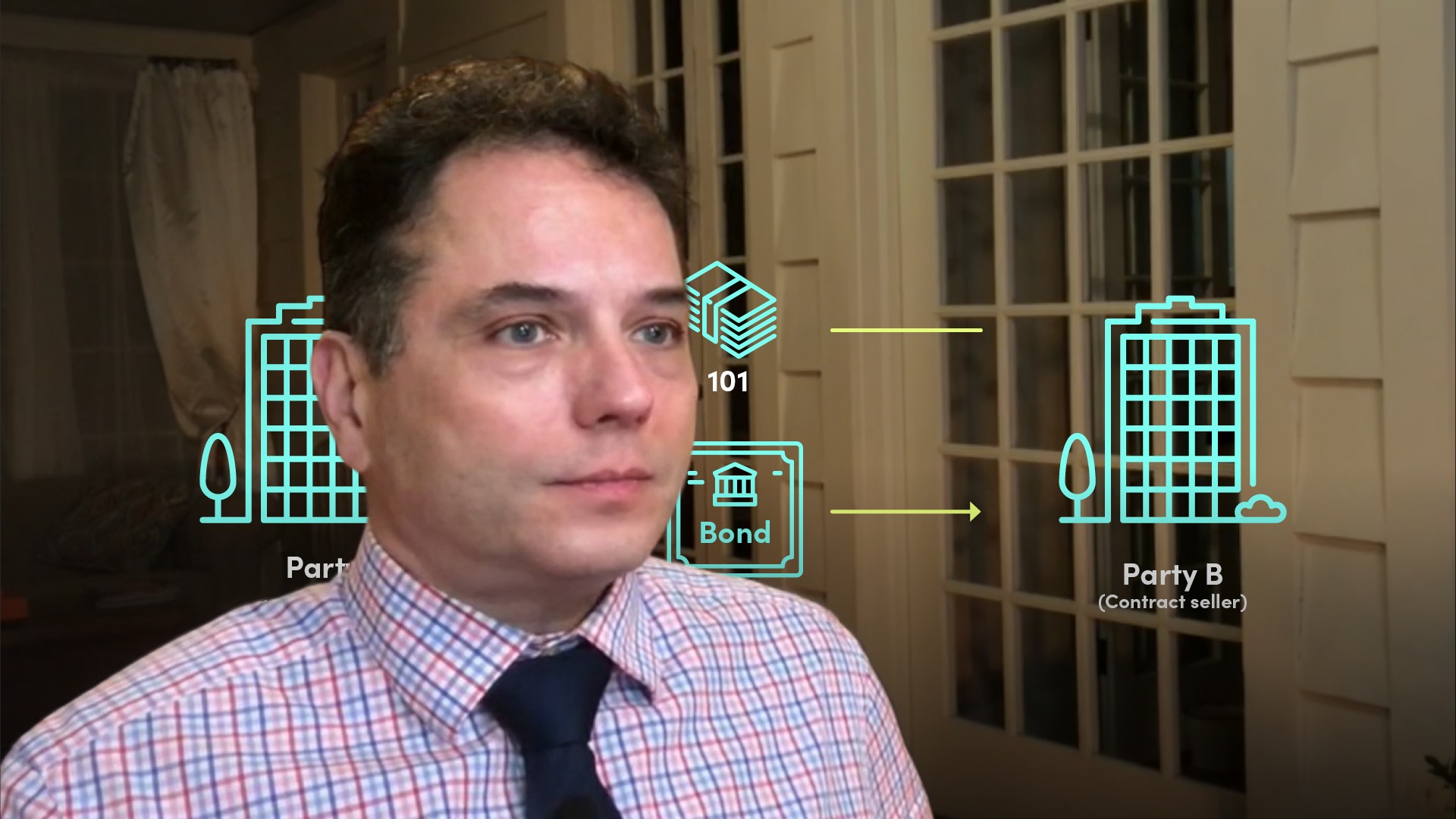

What is the ISDA master agreement?

An initial contract defining this general language, collateral procedures, and all the requirements necessary for both parties to follow and fulfil their agreements.

Forward contracts do not have standard definitions. Over the counter contracts are bespoke party-to-party contracts, which means that they might have agreements that differ from one another. So, to avoid the discrepancies and for everybody to speak the same language, professionals rely on a standardised base of definitions, expressions, language and procedures, which is defined by the ISDA, the International Swaps and Derivatives Association.

Gontran de Quillacq

There are no available Videos from "Gontran de Quillacq"