Dividend Discount Model and Net Asset Value Method

Sarah Martin

30 years: Corporate Valuations

In this video, Sarah continues discussion of equity multiple valuation methods and introduces the dividend discount model and the net asset value method. She will explain why each of these methods are used, illustrate their working and discuss the drawbacks associated.

In this video, Sarah continues discussion of equity multiple valuation methods and introduces the dividend discount model and the net asset value method. She will explain why each of these methods are used, illustrate their working and discuss the drawbacks associated.

Dividend Discount Model and Net Asset Value Method

11 mins 55 secs

Key learning objectives:

Understand the dividend discount model and its drawbacks

Understand the net asset value method and its drawbacks

Understand the scenarios where the net asset value method can be used

Overview:

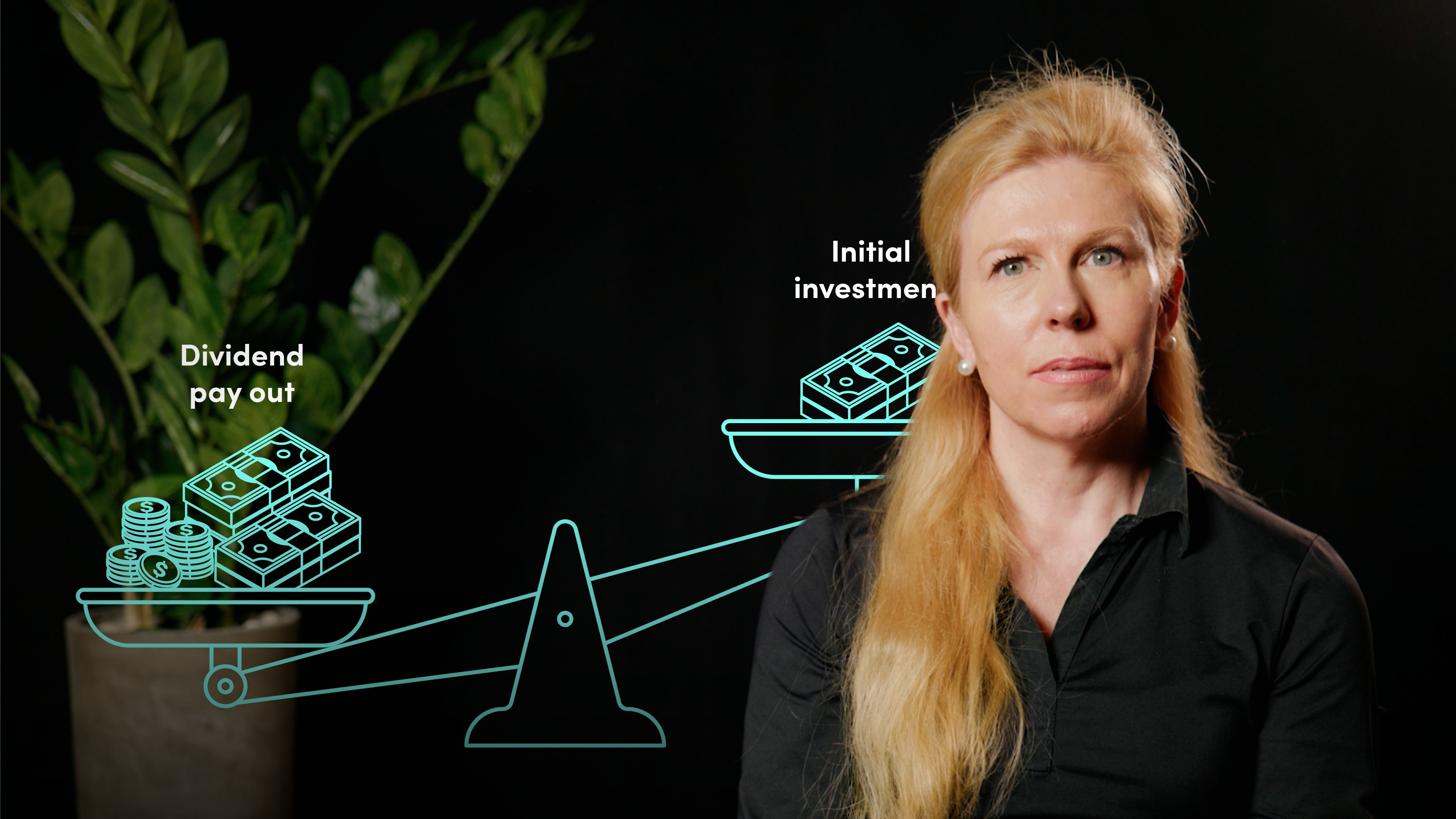

Different types of equity multiples are used based on the user of the valuation and purpose of the valuation. Two of the commonly used methods by practitioners are the dividend discount model and the net asset value method. To gain a holistic view of equity multiples it is important to understand why these methods are used and also see the drawbacks and considerations that need to be kept in mind when using each of these methods.

- Assumes a constant growth rate in dividends. In reality, firms may increase or reduce the growth rate of its dividend pay-out.

- Does not factor in potential rises or falls in the underlying share price.

- The dividend discount method of valuing firms does not work if the firm does not pay a dividend.

- Does not work for firms that are trying to balance growth with also paying a dividend, as growth in net income should also lead to a rise in the share price.

- If interest rates rise, the dividend yield on the stock may become less attractive and investors may be inclined to sell the stock and place their funds in a higher-yielding cash account., leading to a fall in the stock’s valuation.

- Investors buying shares of companies, are not concerned about the value of the underlying assets. They are concerned about the future earnings and cash flows that those assets will generate.

- Book value of equity may materially understate the market value of equity as firms value their assets at historical cost, less depreciation and impairments.

- It cannot be used on brand value which is intangible unless it has been acquired. Thus it cannot be used to reflect the value of internally developed brands.

- Property investment firms – As these firms normally report updated asset values for their property portfolio every 6 to 12 months, the book value of the property company’s assets is normally close to the market value

- Firm due to be liquidated - In this scenario, the book value of assets and liabilities should be revalued to market or liquidation values and the updated net asset value derived.

- Shell companies with no real underlying business either existing or planned and some cash in the bank. In this instance, the valuation could be based on the book value of equity.

- For firms whose market valuation is trading at a discount to its book value of equity. Usually means the market is concerned about the firm’s outlook and is expecting future losses and write-downs.

- Anticipated changes in underlying asset values - Valuation should be adjusted up or down to reflect these changes.

- Tax purposes - If a commercial property company would incur significant tax liabilities from selling its properties, these should be deducted from the valuation.

- Off-balance-sheet liabilities - If there is a more than 50% probability that these may crystallise, then a provision should have been taken and valuers may deduct contingent liabilities.

Sarah Martin

There are no available Videos from "Sarah Martin"