Further Listing Considerations

Kate Craven

35 years: Capital markets

In the first video of this two-part video series, Kate outlined what a listing is and why a listing matters. In this video, she looks further into the topic by first discussing the assessment issuers should make when deciding which stock exchange to pick. She then explains the requirements for listings and finishes up with a further discussion on the changes emerging due to Brexit.

In the first video of this two-part video series, Kate outlined what a listing is and why a listing matters. In this video, she looks further into the topic by first discussing the assessment issuers should make when deciding which stock exchange to pick. She then explains the requirements for listings and finishes up with a further discussion on the changes emerging due to Brexit.

Further Listing Considerations

7 mins

Key learning objectives:

Identify considerations as to which stock exchange to use

Understand what is required for a listing

Learn what changes have happened since Brexit

Overview:

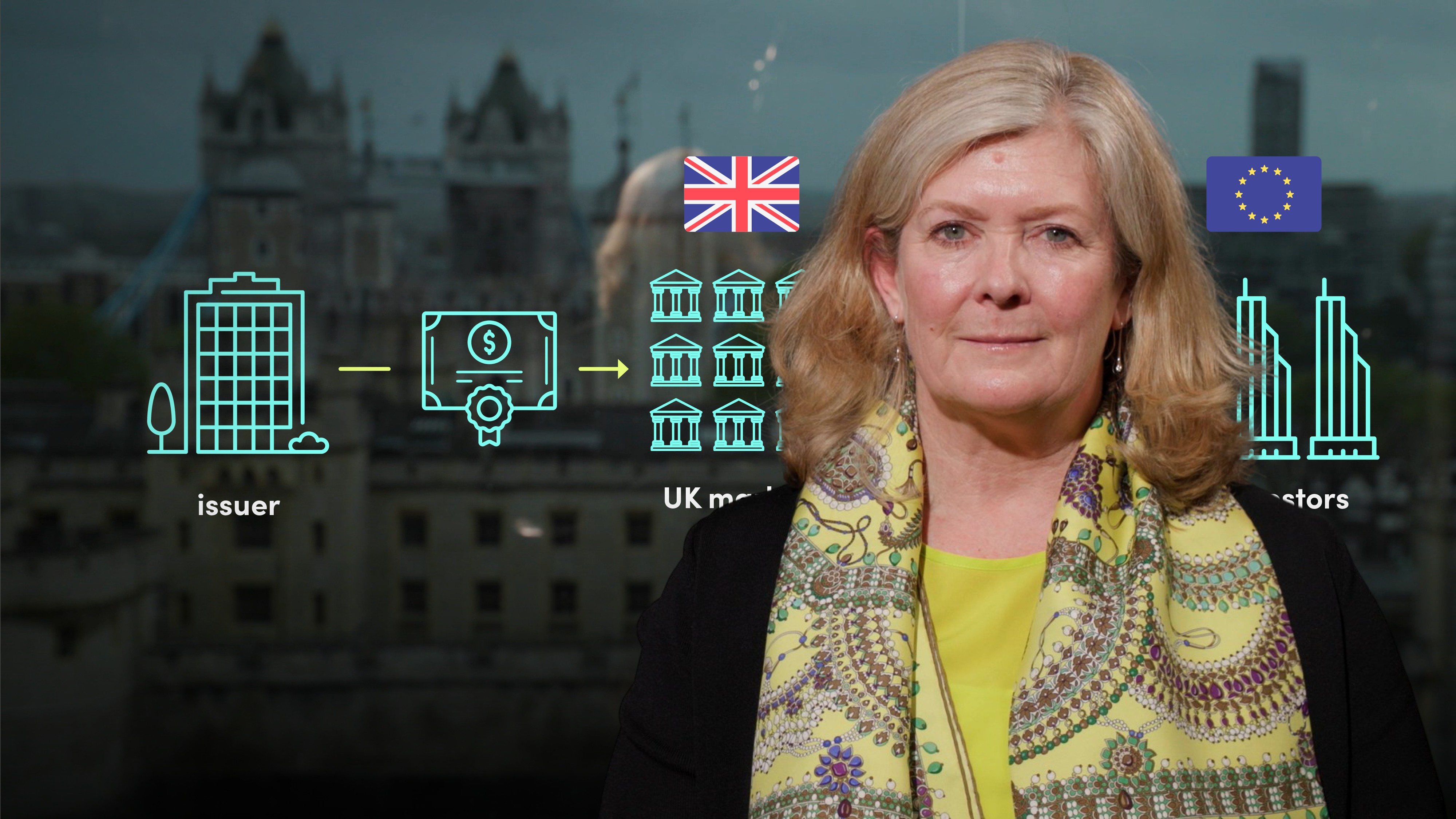

A listing means that an offering document (or prospectus) for an issue of debt or equity securities has been reviewed and approved by a stock exchange, and the securities are admitted to trading on that exchange. The issuer will have to determine the appropriate stock exchange to pick as there are some variations between them and the issuer will also have to understand what is required for a listing.

Which stock exchange to pick?

EU regulated markets all follow the same disclosure, therefore there is little difference between them other than turn-around times, speed of review and ease of contacting them. Some stock exchanges also require that issuers use a listing agent.

As English is the most commonly used language, it is a good idea to select a stock exchange that can review documents written in English.

Most European issuers as well as some issuers based outside the EU will already have an equity listing in the EEA and are therefore already subject to the ongoing disclosure requirements associated with that, for such issuers, it will be relatively simple to comply with the continuing obligations for any debt securities listed on the same stock exchange

What is required for a listing?

To list on an EU regulated market, a two-year trading record with financial information consistent with IFRS is required for a listing as well as a listing document (prospecuts) that complies with the EU Transparency Directive.

If an issuer does not have a two-year trading record they may wish to list on an exchange regulated market.

Some issuers access the market by setting up a Medium Term Note Programme. The offering document (base prospectus) for a programme, once approved, is valid for a 12-month period. As this base prospectus has already been approved there is no requirement for the relevant stock exchange to review the final terms for each drawdown under the programme, speeding up market access.

What has changed since Brexit?

Currently the UK Prospecuts Regulation substantially mirrors the EU Prospectus Regulation, however there are already indications of divergence. However, it is essential for issuers listing in the UK that exepmtipns are aligned so that they can continue to offer wholesale deals on a cross-border basis as seamlessly as possible.

Although an EU listing allows issuers to passport their prospectus into other EU member states, this is rarely done. It therefore seems unlikely that issuers will move away from a London listing to a listing elsewhere in the EU, particularly since the disclosure requirements are broadly still aligned under the EU and UK Prospectus Regulations.

Kate Craven

There are no available Videos from "Kate Craven"