Group and Operating Enterprise Valuation

Sarah Martin

30 years: Corporate Valuations

In this video, Sarah delves deeper into EV multiple valuations and then explains the difference between operating enterprise value and group enterprise value (total enterprise value) and how to calculate the correct underlying multiple.

In this video, Sarah delves deeper into EV multiple valuations and then explains the difference between operating enterprise value and group enterprise value (total enterprise value) and how to calculate the correct underlying multiple.

Group and Operating Enterprise Valuation

8 mins 20 secs

Key learning objectives:

Understand the difference between operating EV and total EV (group EV)

Understand the adjustments to calculate the correct underlying EV/EBITDA multiple

Understand the complications caused by NCIs in calculating EV multiples

Overview:

The enterprise value of a firm is the value of the whole business (equity value plus the net debt and equivalents). Applying a multiple to enterprise valuations allows us to get around some of the problems involving equity multiples such as lack of comparable capital structure.

Enterprise value (EV) of a firm represents the value of the entire business before net debt and equivalents are subtracted. It's the combined total of equity value and net debt, akin to the full purchase price needed to acquire the entire company, including its assumed debt. This concept can be likened to purchasing a house, where the market value of the house is similar to the EV of a business. Looking at EV is particularly useful when planning changes to the target firm's capital structure or when comparing firms with different capital structures, as it provides a clearer picture than equity valuations alone.

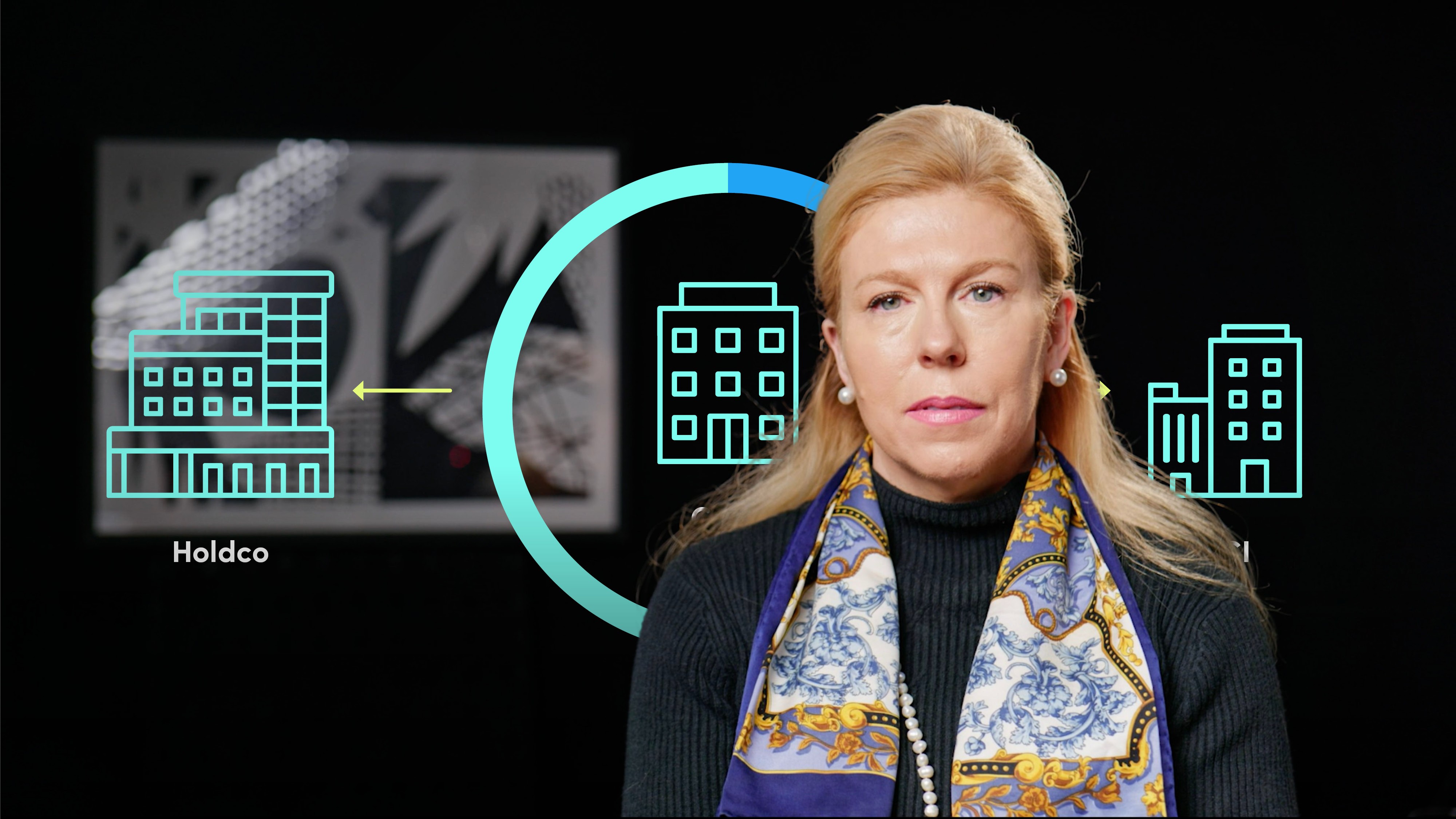

What is the difference between operating EV and total or group EV?

There are two primary types of enterprise value to consider: operating enterprise value and total or group enterprise value. Operating EV pertains to the value of the core operating units, calculated based on the EBITDA these units generate. Conversely, total or group EV includes the market value of additional assets that do not contribute to EBITDA, like surplus land or non-core investments. These assets, while not part of the operating business, still hold value for shareholders and must be considered in the overall valuation. Understanding this distinction is crucial when determining the correct multiple for the core business, which should be based on the operating EV.

How do we adjust to calculate the correct underlying EV/EBITDA multiple?

To calculate the accurate underlying EBITDA multiple for a business, we must exclude non-operating assets from the market capitalisation and enterprise value. Non-operating assets like surplus land or shares in joint ventures may inflate the EV but do not contribute to EBITDA, thus skewing the multiple upwards. By deducting the value of these assets from the market capitalisation, we obtain a more accurate representation of the underlying business. This ensures that the EBITDA multiple reflects only the core operating assets and activities.

What complications are caused by non-controlling interests (NCIs) in calculating EV multiples?

Non-controlling interests (NCIs) add complexity to EV calculations as they represent stakes in subsidiary companies owned by investors other than the parent company's shareholders. The equity market value of the holding company is often reduced because shareholders do not own 100% of the subsidiaries. However, the reported EBITDA usually reflects 100% of the subsidiaries' earnings, creating a mismatch. To address this, the market value of the NCI should be added to the equity value, aligning the numerator and denominator in the EV/EBITDA ratio to ensure both reflect 100% of their respective values. This adjustment helps achieve consistency in comparing enterprise value with EBITDA.

Sarah Martin

There are no available Videos from "Sarah Martin"