Overview of MREL

Gilles Renaudiere

Corporate Advisor: BNP Paribas

In this video, Gilles explains why banks need bail-in debt, and outlined MREL, or Minimum Requirements for Own Funds and Eligible Liabilities, which is the EU’s version of bail-in debt.

In this video, Gilles explains why banks need bail-in debt, and outlined MREL, or Minimum Requirements for Own Funds and Eligible Liabilities, which is the EU’s version of bail-in debt.

Overview of MREL

11 mins 56 secs

Key learning objectives:

Understand the concept of bail-in capital, specifically through the lens of MREL

Understand why bail-in capital is required, even with increased capital requirements

Outline how the MREL level is determined within banks and how this has evolved over time

Overview:

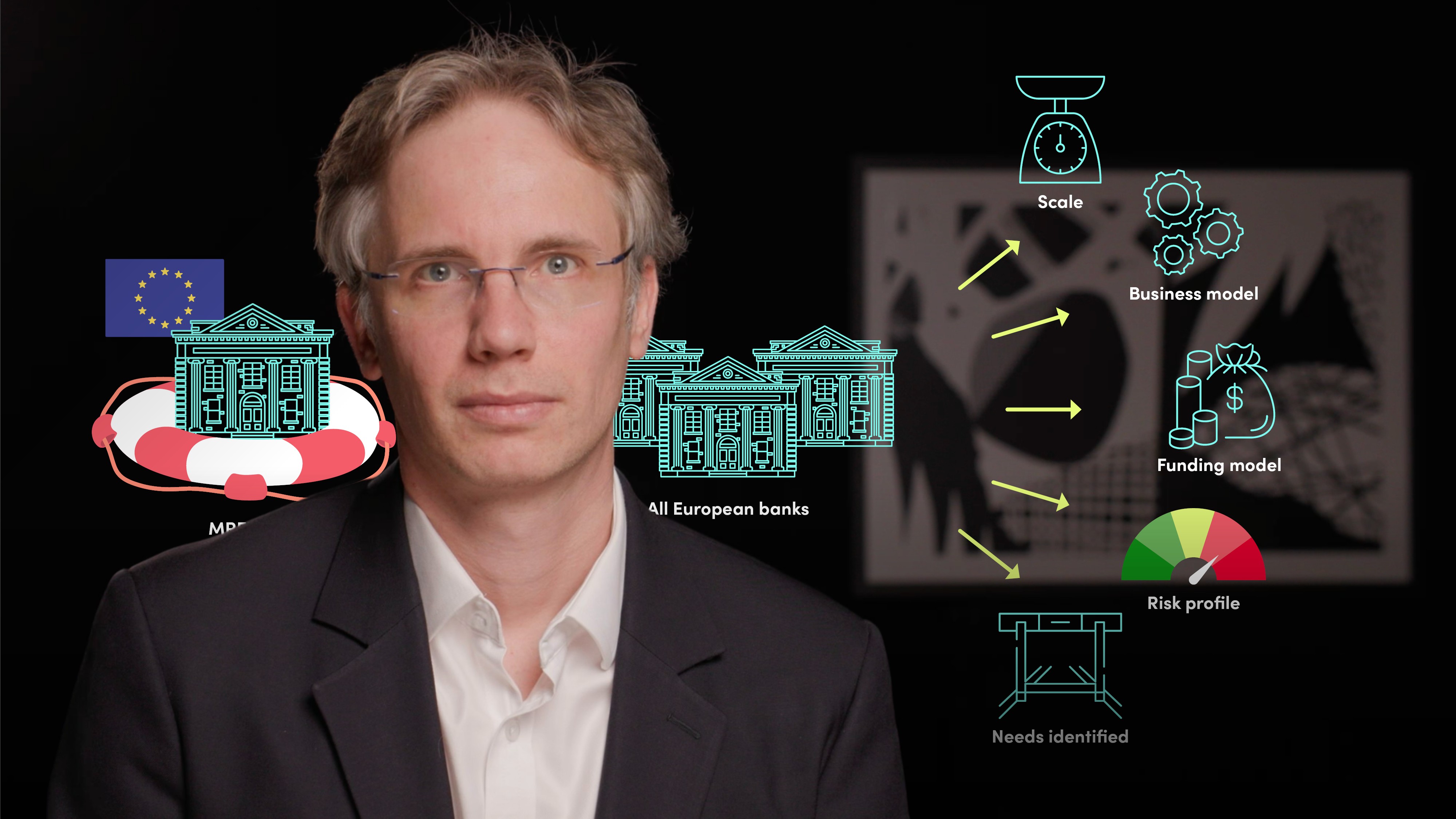

Bail-in debt emerged after the global financial crisis as a way to secure banks' financial stability in the event of a crisis. This tool, established through MREL (Minimum Requirement for Own Funds and Eligible Liabilities) and TLAC (Total Loss-Absorbing Capacity). MREL, or Minimum Requirement for Own Funds and Eligible Liabilities, was introduced in the EU in 2014 to ensure an effective and credible application of the bail-in tool. It is applicable to all EU banks and is individually tailored based on factors such as size, business model, and risk profile. MREL targets are set by EU resolution authorities and are based on the bank's capital requirements and agreed resolution strategy. The LAA is equal to the capital requirement of the bank, and the recapitalisation amount is based on the bank's resolution strategy.

Why is bail-in capital required, even with increased capital requirements?

Increased capital requirements aim to reduce the likelihood of bank failures, but they cannot guarantee it won't happen. In the event of a bank failure, bail-in capital can be used to recapitalise the bank, rather than relying on taxpayers or the government. This helps to maintain stability in the financial system and prevent losses to depositors and taxpayers.

What is the bail-in tool, and what is MREL?

The bail-in tool is a power that national authorities can use to handle failing banks without requiring a taxpayer bailout. The tool allows long-term wholesale debt issued by banks to be transformed into equity in a crisis to allow for recapitalisation without public sector support.

The EU introduced the bail-in tool via the BRRD in 2014 and established the Minimum Requirement for Own Funds and Eligible Liabilities (MREL) to ensure an effective application of the bail-in tool. MREL is a minimum requirement for own funds and eligible liabilities, tailored to banks based on their size, risk profile, and other factors.

How is a bank’s MREL target determined and how has it evolved over time?

In BRRD I, MREL was originally expressed as a percentage of a bank's total liabilities and own funds and consisted of two ratios: a risk-weighted and a non-risk-weighted requirement, both of which consisted of the sum of a loss absorption amount and a recapitalisation amount. The loss absorption amount was equal to the capital requirement of the bank, while the recapitalisation amount was based on the bank's resolution strategy.

BRRD 2 introduced changes to MREL calculation to make it more consistent with the TLAC standard. MREL is now calculated by reference to a risk-based ratio and a non-risk-based ratio, based on risk-weighted assets and leverage ratio exposure. BRRD II required G-SIBs to meet a minimum TLAC requirement of 16% risk-based ratio or 6% non-risk-based ratio, which rose to 18% and 6.75% respectively in 2022. Top tier banks with over €100bn assets must meet a 13.5% risk-based and 5% non-risk-based ratio. For other financial institutions, MREL is set by local resolution authorities using LAA and RCA.

Gilles Renaudiere

There are no available Videos from "Gilles Renaudiere"