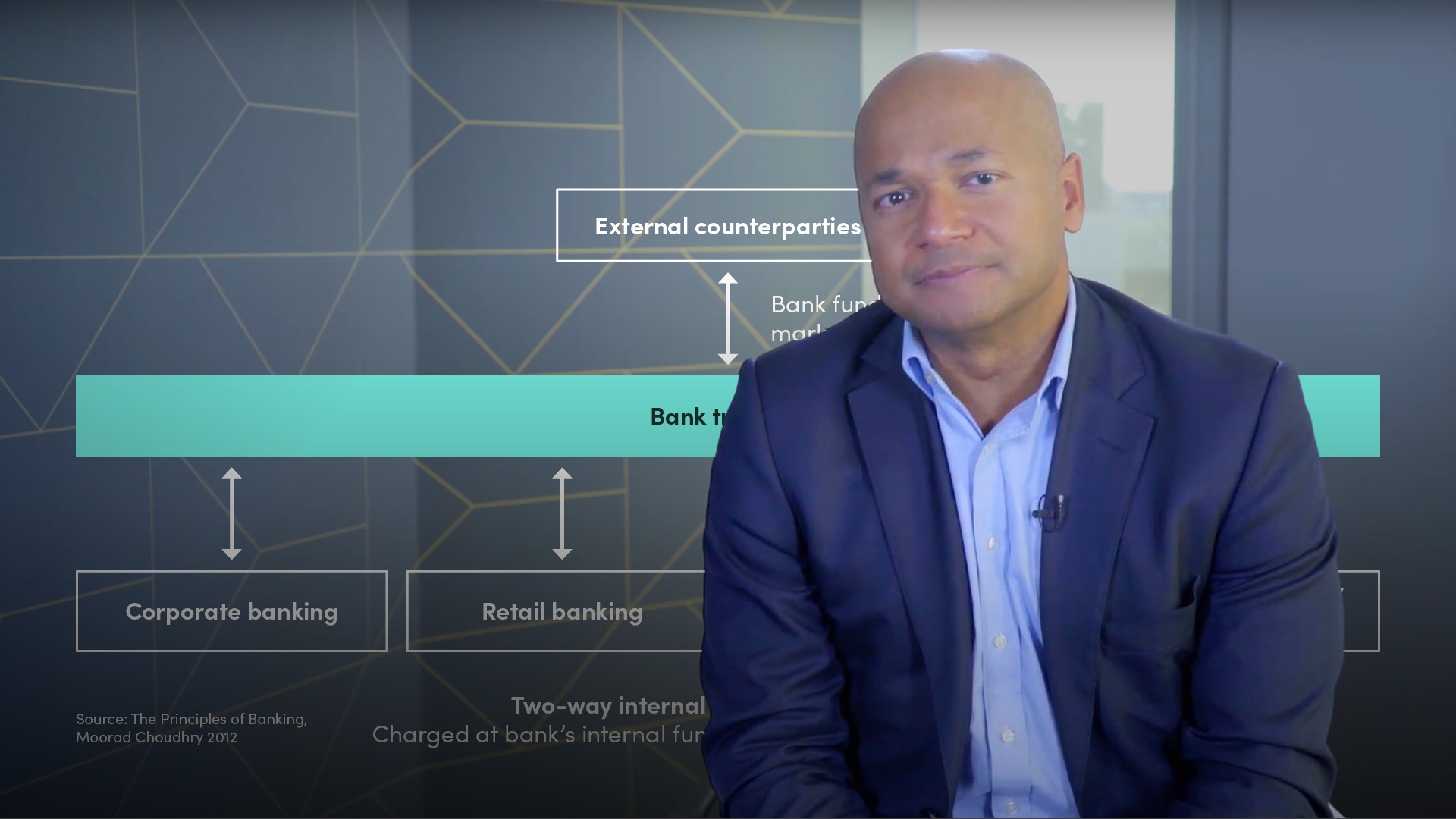

Transfer Pricing

Transfer pricing is concerned with the prices charged by one party in a transaction to a connected party. The international transfer pricing mechanisms used by multinational corporations have attracted significant attention in recent years and led to transfer pricing legislation to prevent multinationals abusing transfer pricing (i.e. charging prices that would not have been charged if the parties were not connected) to minimise taxation. OECD member countries have adopted the so-called Arm’s Length Principle to create a fair division of multinational profit taxation. This says that transactions between connected parties should be treated for tax purposes by reference to the amount of profit that would have arisen if the same transactions had been executed by unconnected parties.