Glossary

Technical FoundationsVega

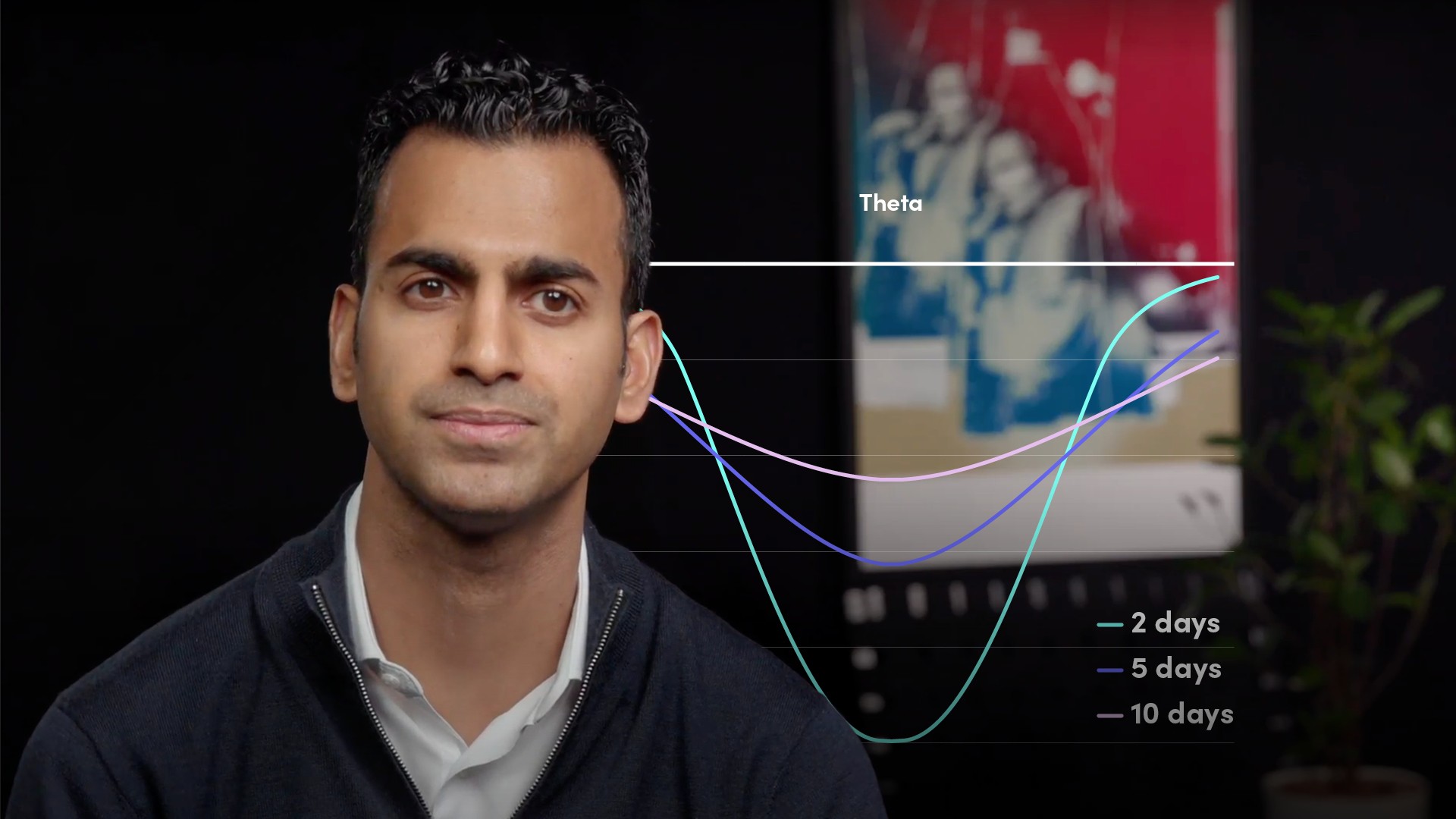

Vega, one of the so-called option Greeks (along with Gamma, Delta, Theta etc), is a measure of how sensitive the price of an option is to a 1% change in the implied volatility of the underlying.

Vega

Vega, one of the so-called option Greeks (along with Gamma, Delta, Theta etc), is a measure of how sensitive the price of an option is to a 1% change in the implied volatility of the underlying.